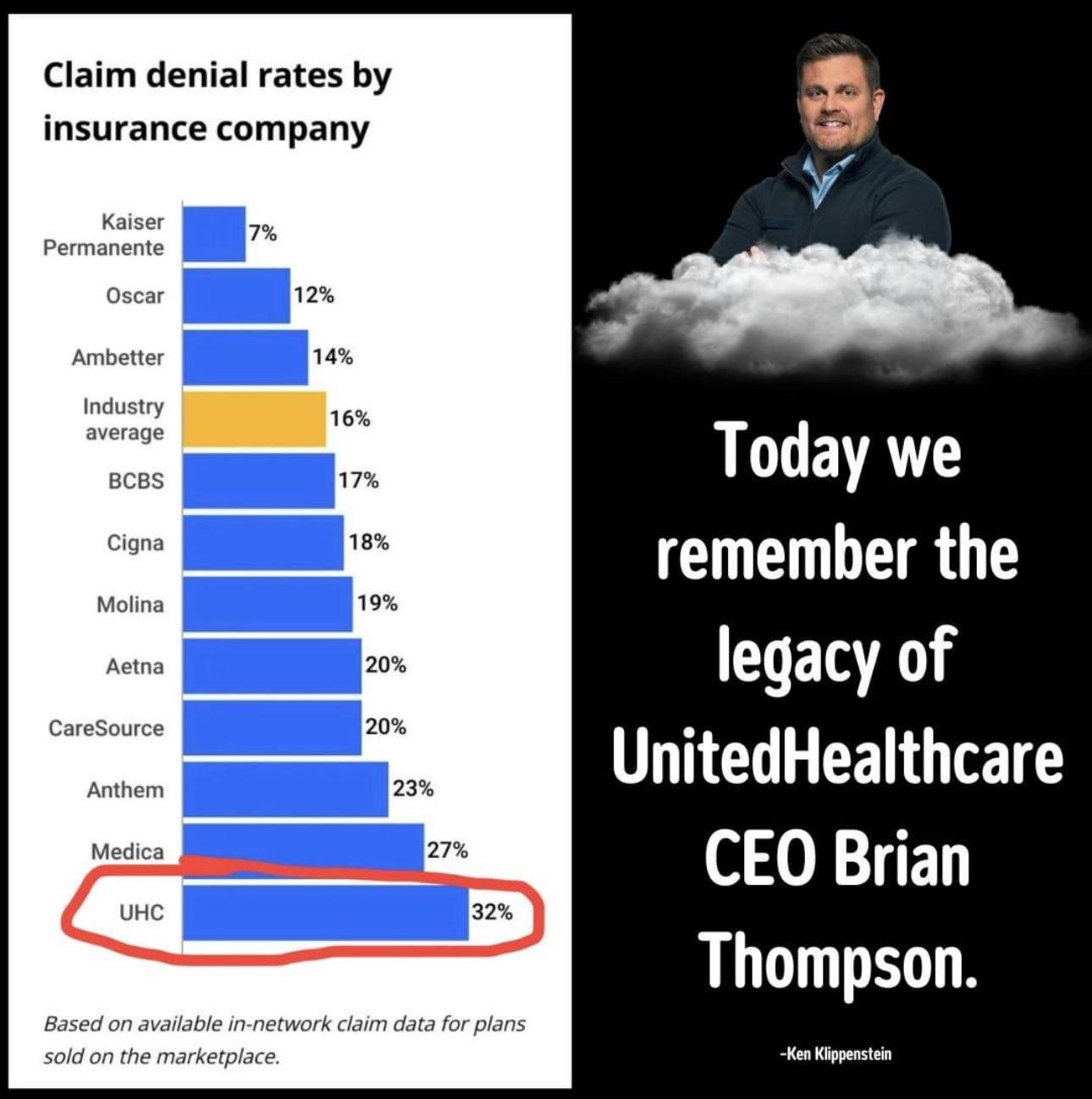

My main concern with Kaiser is that it severely limits the pool of covered doctors and specialists. All the Kaiser plans I’ve seen also have higher out-of-pocket maxima with zero out-of-network coverage.

Covered doctors and specialists… out of network… people on Reddit kept telling me my socialised universal multi-payer healthcare by statutory health insurance, would mean I could not see the doctor I wanted and would wait forever for services. And sure, for everything that’s not immediately necessary I do wait some time. But for all things acute I can go to any general practitioner who will either provide immediate help or forward me to a specialist for immediate help. No matter where in my country I am, no matter which hospital, GP or specialist I go to, everything important is covered. And I pay less per month for it than Americans do.

The limited of out-of-network coverage is kind of the point of Kaiser. There are some times that they’ll do it if they’ve understaffed in a specialist’s area, if it’s emergency / trauma care, etc. But the main point is to try to keep things within the non-profit network, and to limit the cost creep imposed by the for-profit healthcare providers.

As for out-of-pocket, that really depends on the plan you’re buying or your employer is negotiating. When I was picking a Kaiser plan, I was usually choosing between similar PPO offerings with comparable out-of-pocket.

My wife and I, and many of her insurance coworkers, have found that the PPO plans often hide the costs. It looks good on paper at first, but the TOS about what is and isn’t covered can often be much more profit-driven in the PPO space. And you often don’t learn about these details until you need care or a medication.

{kind=link}

My main concern with Kaiser is that it severely limits the pool of covered doctors and specialists. All the Kaiser plans I’ve seen also have higher out-of-pocket maxima with zero out-of-network coverage.

Covered doctors and specialists… out of network… people on Reddit kept telling me my socialised universal multi-payer healthcare by statutory health insurance, would mean I could not see the doctor I wanted and would wait forever for services. And sure, for everything that’s not immediately necessary I do wait some time. But for all things acute I can go to any general practitioner who will either provide immediate help or forward me to a specialist for immediate help. No matter where in my country I am, no matter which hospital, GP or specialist I go to, everything important is covered. And I pay less per month for it than Americans do.

Out of curiosity, what country?

Don’t worry, we already know… None of it makes sense in any context besides “making money for corporations and wealthy stock holders”

The limited of out-of-network coverage is kind of the point of Kaiser. There are some times that they’ll do it if they’ve understaffed in a specialist’s area, if it’s emergency / trauma care, etc. But the main point is to try to keep things within the non-profit network, and to limit the cost creep imposed by the for-profit healthcare providers.

As for out-of-pocket, that really depends on the plan you’re buying or your employer is negotiating. When I was picking a Kaiser plan, I was usually choosing between similar PPO offerings with comparable out-of-pocket.

My wife and I, and many of her insurance coworkers, have found that the PPO plans often hide the costs. It looks good on paper at first, but the TOS about what is and isn’t covered can often be much more profit-driven in the PPO space. And you often don’t learn about these details until you need care or a medication.

So it’s the vertical integration.